Cozzy is in open beta: a friendlier money app for Ireland

By Cozzy · Published June 2026 · Last reviewed June 2026 · Sources verified against primary references as of June 2026.

Forty-three percent of adults in Ireland don't meet the minimum threshold for basic financial literacy (Department of Finance, 2025). One in eight could only cover their costs for a month or less if their income stopped tomorrow (CCPC, 2024). If you find money harder than it should be, you're very much not alone.

We've been building Cozzy for some time now. Finally we're at the point of opening the doors to anyone who wants in. Cozzy is now in open beta on TestFlight and Google Play, and this post is the proper introduction to say hi, tell you what Cozzy is all about and hopefully get you interested.

What is Cozzy?

Cozzy is an Irish personal-finance app for people who want to feel calmer about money, not more guilty. It combines a budgeting tool, a goals tracker, a built-in AI coach called Olivia, and a learning library tuned to Ireland.

The short version: we're trying to make the basics of money feel learnable, manageable, and a little bit gentler, especially for people who never quite got taught this stuff in school, which judging by our chats with our peers is all of us.

Why are we building this?

Ireland has a financial-literacy gap, and it's not the cliché you might expect. People here do try. Eighty-six percent of households save in some form, mostly through deposit accounts (CCPC, 2024). What's missing is confidence with the underlying ideas. Fewer than 40% of Irish adults who hold a savings, investment or retirement product can correctly answer a basic question on compound interest (CCPC, 2024).

In early 2025, Ireland published its first national financial literacy strategy.

"Financial literacy is an important life skill that promotes individual financial resilience and wellbeing."

Paschal Donohoe, Minister for Finance. Source: Department of Finance press release, February 2025.

The OECD framed it more directly in the same release:

"In today's financial marketplace, possessing adequate levels of financial literacy is not a luxury, but a fundamental life-long skill."

Yoshiki Takeuchi, OECD Deputy Secretary-General. Source: Department of Finance, 2025.

That's the gap we're trying to help close, one small useful interaction at a time.

The cost-of-living backdrop is the other half of the picture. Around 45% of Irish households reported at least some difficulty making ends meet in 2025, and 36.9% had no money left to set aside at the end of the month (CSO SILC 2025). When margins are this tight, a clear plan isn't a luxury. It's the thing that keeps the month from becoming an emergency.

What is in the open beta?

There are four things we want you to try first.

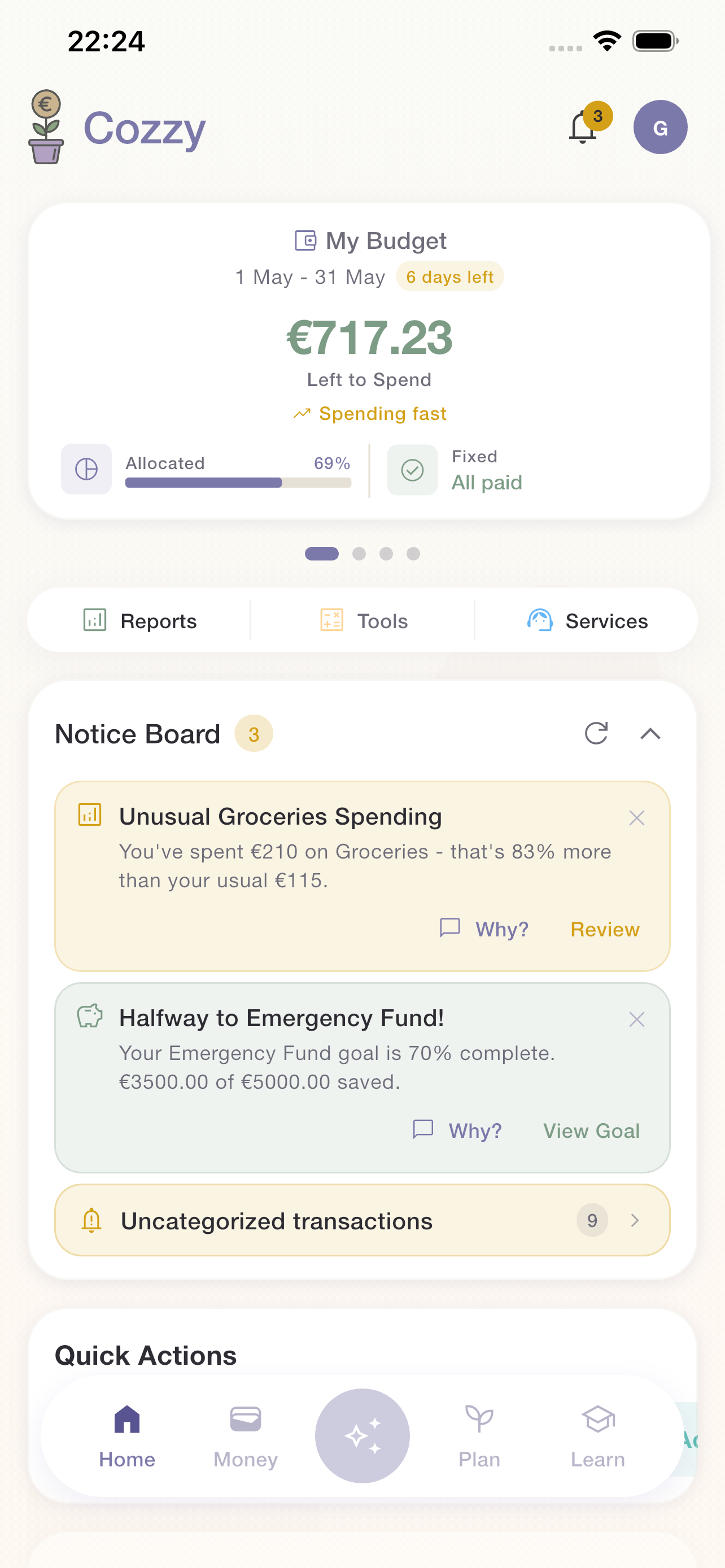

1. A budget that actually fits a real life

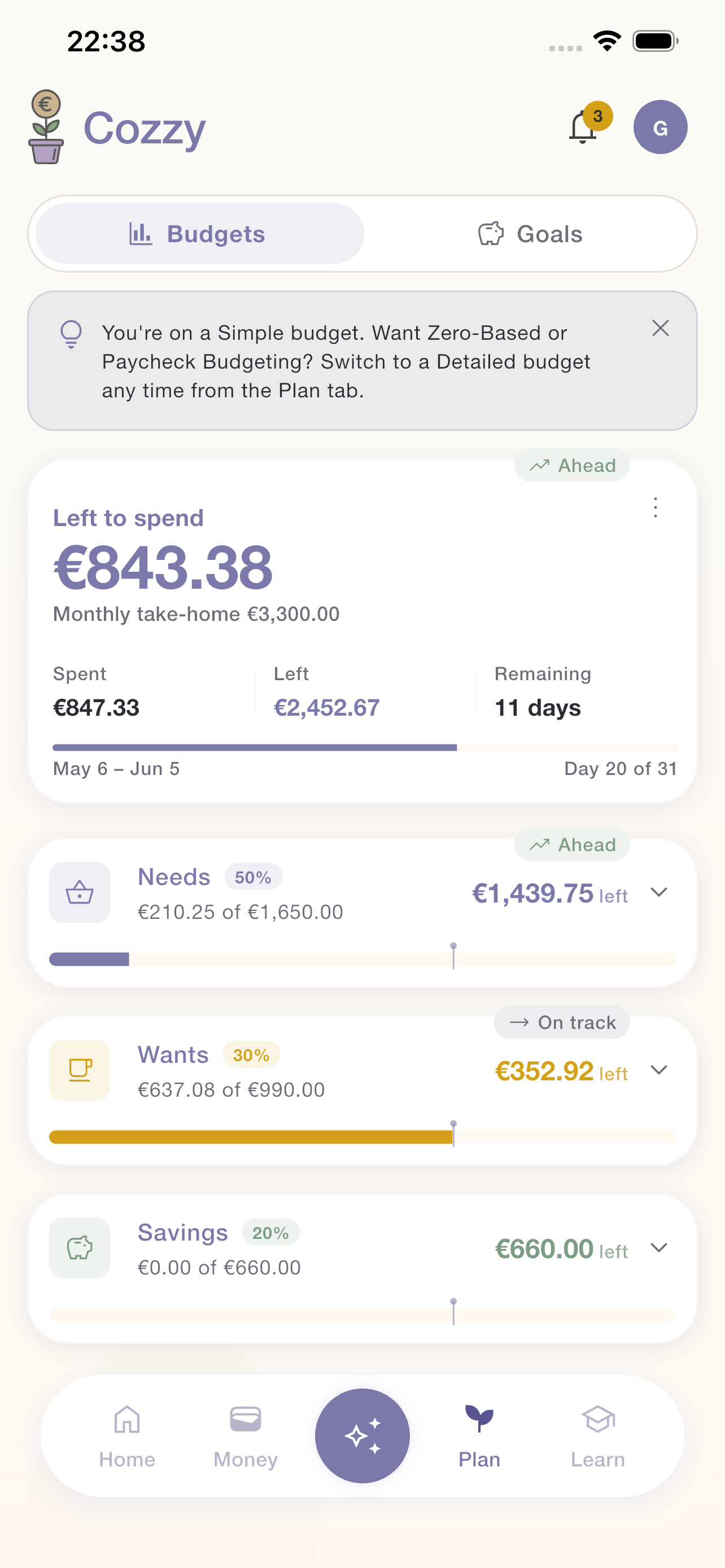

You set your monthly take-home, split it across Needs, Wants and Save, and Cozzy tracks how much of each is left and how many days are in the cycle. You can stay on a simple percentage budget or switch to zero-based or paycheck budgeting any time. Fixed bills like rent and utilities are scheduled in advance, so you can see exactly what is still spendable.

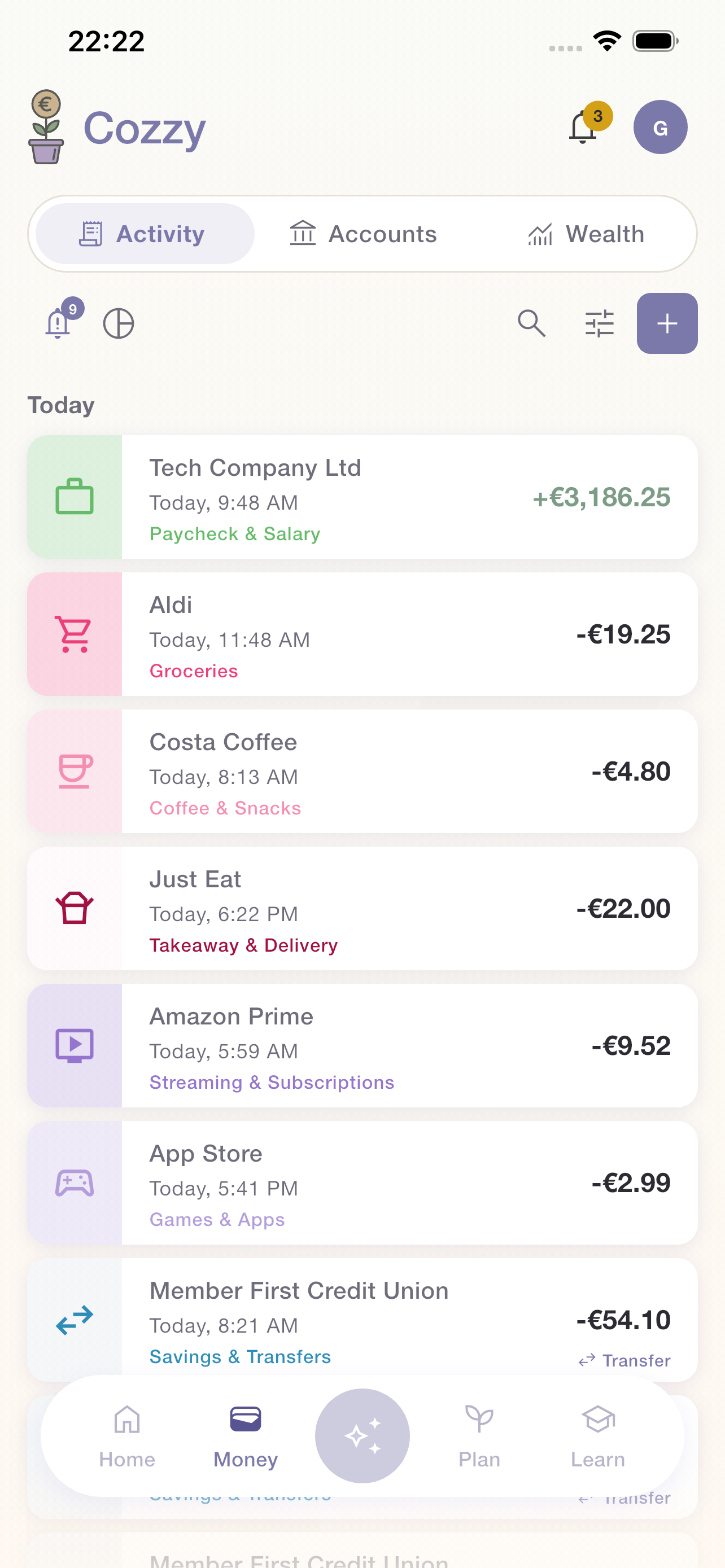

Underneath the budget is a clean activity feed — every transaction is grouped by day, each one tagged with a category that drives the bucket totals you saw above. In open beta you add these manually (bank linking is on the way), but the categorisation, search and Olivia hooks ("Monthly spending", "Budget check") are all live.

Cozzy intentionally focuses on what's still possible this month, not on grading what went wrong last month. To be fair, some people genuinely do better with a sharper "you're spending too much" signal, and we'll keep evolving the nudges as we hear from real users.

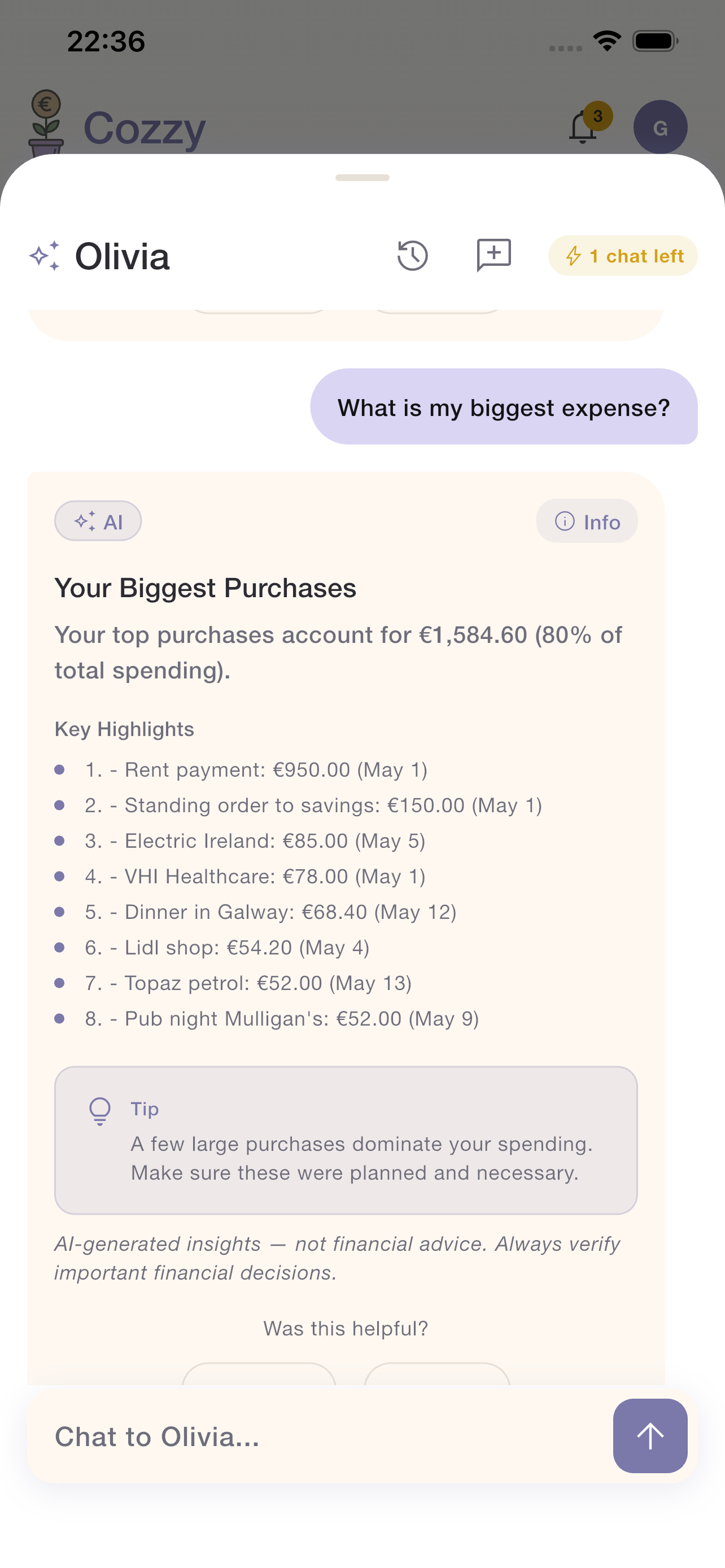

2. Olivia, an AI coach who admits when she doesn't know

Olivia is Cozzy's in-app coach. You can ask her preset questions like "is my budget realistic?" or type your own, and she replies in plain language with what she can see in your data, and importantly, what she can't.

That second part matters. Most financial conversations go off the rails when someone gives you confident advice based on missing information. We've spent a lot of time designing Olivia to say when she needs more data, suggest the next useful question, and never invent a number she can't trace back to your accounts or your inputs. If she doesn't know, she'll say so.

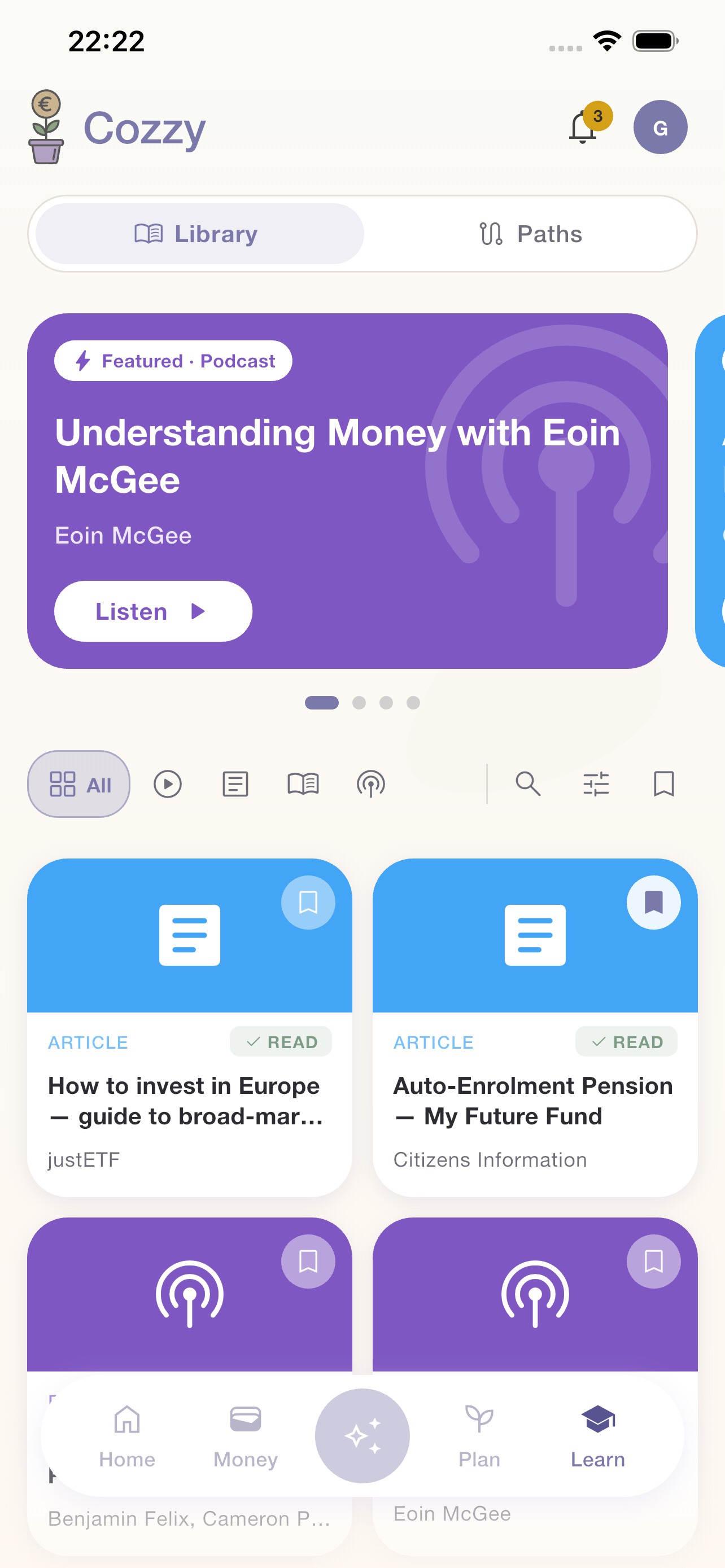

3. A learning library built for Ireland

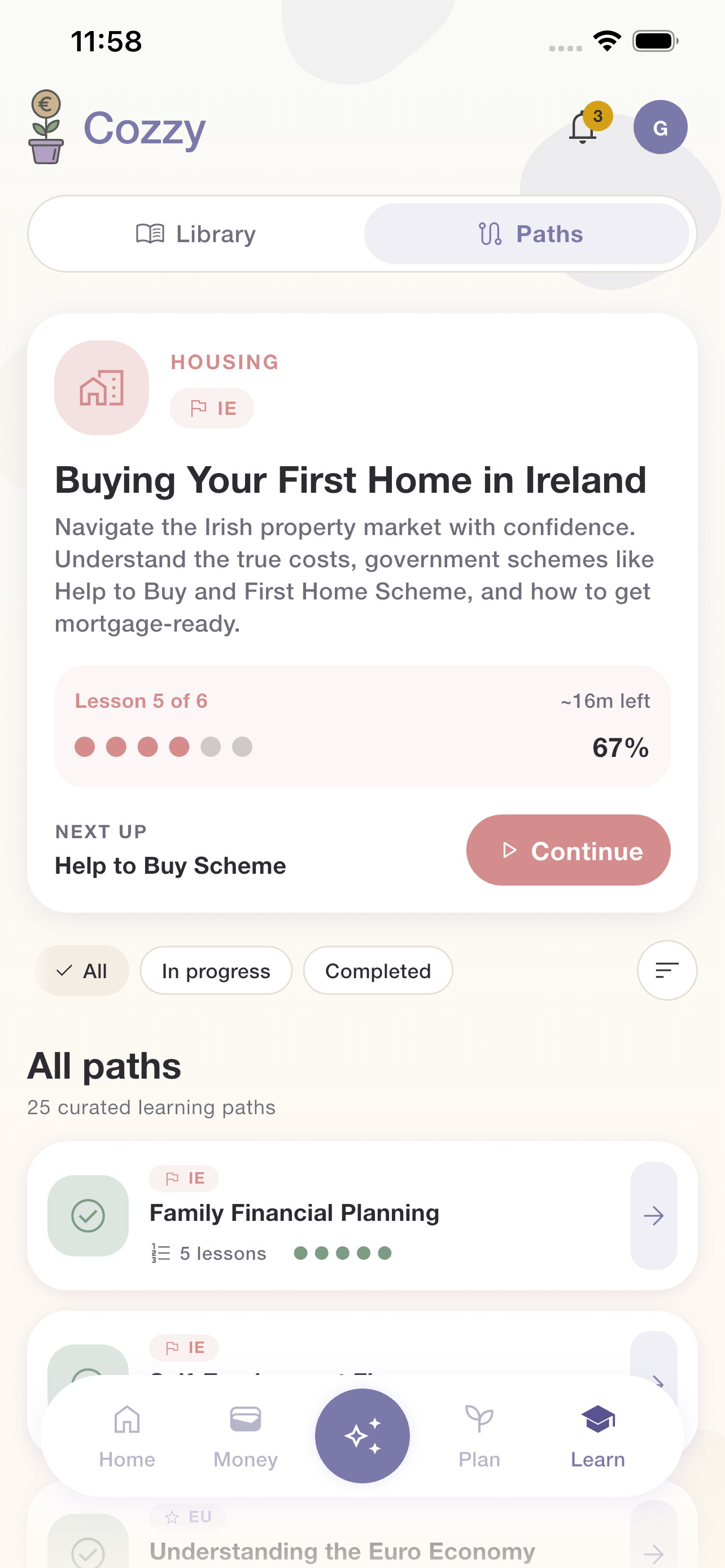

The Learn tab pulls together short articles, books and structured learning paths. Think the kind of bite-sized content that fits into a coffee break. Topics are curated for an Irish audience: auto-enrolment, payments to families, credit unions, PRSAs, mortgages.

If you prefer to learn in a sequence rather than dipping in and out, the Paths tab is built for that. Each path is a curated set of lessons that builds on the last one, so you can start at Money Foundations and work up to investing or pensions when you are ready.

The pension-auto-enrolment moment is a useful frame for why this matters. As Minister Heather Humphreys put it when Ireland's My Future Fund commencement order was signed:

"Auto Enrolment is the single most significant reform of the pensions landscape in Ireland since the introduction of the State Pension in 1908."

Heather Humphreys, Minister for Social Protection. Source: Department of Social Protection, October 2024.

Around 800,000 workers are being brought into pension saving for the first time (DSP, 2024). Most of them will want to understand what's being taken out of their payslip and what it buys them. We want Cozzy to be a calm, accurate place to figure that out.

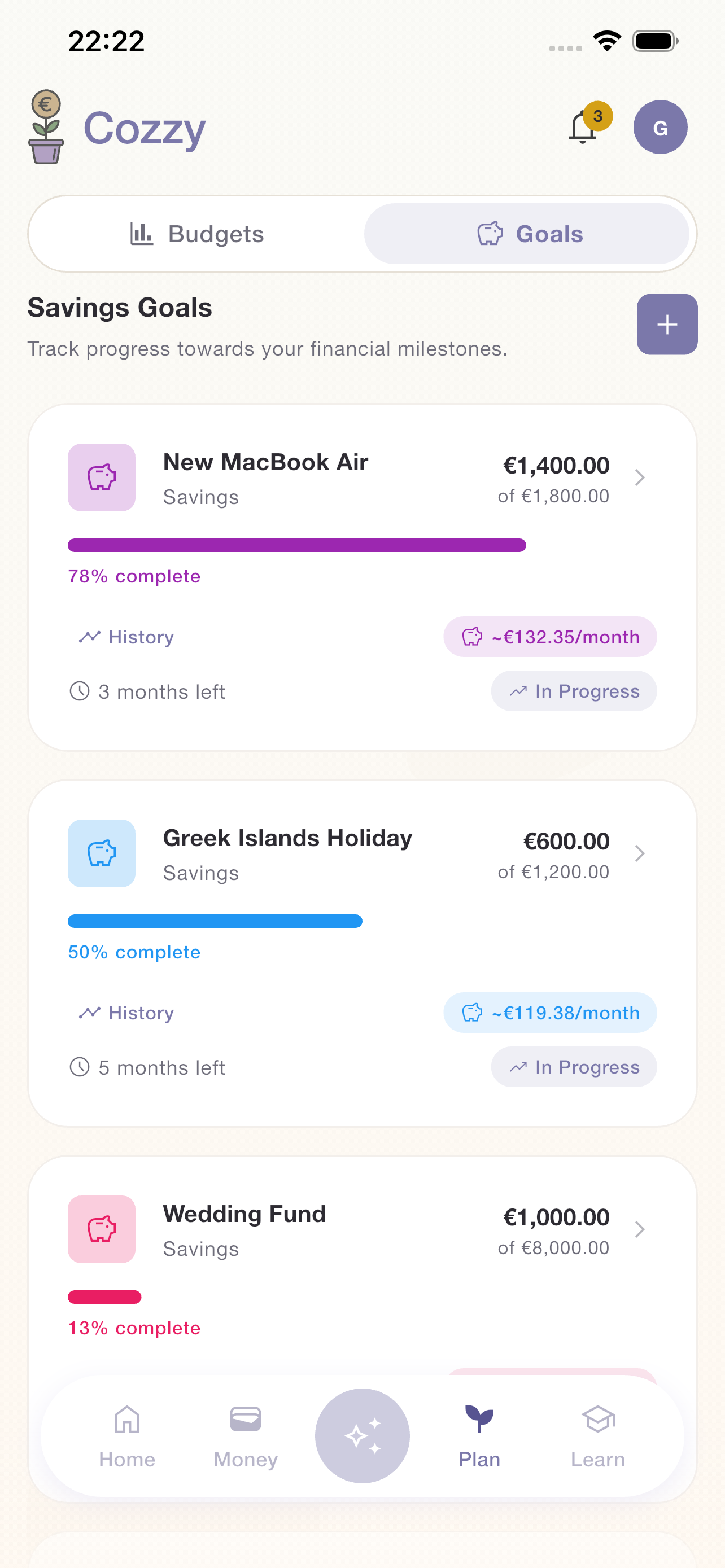

4. Goals you can actually believe in

You can set up savings goals (emergency fund, holiday, first car, deposit) and Cozzy tracks your pacing against them. The pacing chip shows On track, Ahead or Behind in plain words, with an icon that matches the label rather than the underlying status code.

What is not in the open beta yet?

We'd rather say this out loud than have you find it the hard way.

- Automatic bank linking isn't live yet. We're using Yapily for open-banking connections, and the full integration is gated until our launch later this year. In open beta you can add transactions manually, or work entirely from your budget and goals without transaction tracking. Olivia will tell you honestly when she doesn't have enough data to answer a question. That's by design.

- Net worth, holdings, and liabilities are visible as cards on the home screen, but will mostly show zeros until bank linking is enabled.

- A handful of Pro-tier features are visible but soft-gated behind a "coming soon" chip while we finish them.

We thought hard about waiting until everything was perfect. In the end, getting Cozzy into real hands, with the open-beta limitations clearly named, felt more useful than another quiet quarter.

Who is Cozzy for?

Cozzy is built primarily for people in Ireland who:

- Want a budget that fits a real Irish payday, including four-weekly pay cycles and the usual mix of fixed bills.

- Prefer a calmer tone, where the focus is on what is still possible this month rather than what has gone wrong.

- Want a single place that combines budgeting, goals, a coach and learning content, rather than juggling four separate apps.

- Want learning content that's actually relevant to Ireland. Plenty of books, podcasts and articles are fantastic if you're British or American; Cozzy's content is built for an Irish audience.

It's fair to say Cozzy is not the right fit for everyone. If you live in a spreadsheet and want maximum data-export power and custom rules, you'll hit our limits in the open beta. If you want fully-automated bank syncing today, you'll want to revisit at full launch. If you prefer a strict, deficit-led tracker that emphasises what you should have done differently last month, our gentler framing may not suit you, and that's completely fine. Personal-finance tools work because they fit how you think. We're designing Cozzy for the people who, like a lot of us at the company, found the deficit framing more discouraging than helpful.

How to join the open beta

It's free on both iPhone and Android. The latest TestFlight and Google Play links are always on cozzy.io, so head there to join.

If you'd rather wait for full launch, drop your email at cozzy.io and we'll let you know the moment bank linking is live.

What you can do this week, beta or not

A few small steps that work whether you install Cozzy or not. The CCPC made the point well:

"Knowledge is power and financial education is protection."

Kevin O'Brien, Commission Member. Source: Competition and Consumer Protection Commission, November 2024.

- Write down what arrives and what leaves in a typical month. Even on paper. The act of writing it down beats most apps.

- If you've started auto-enrolment, look at your payslip and find the line item. Knowing exactly what's being deducted makes it feel less abstract.

- Pick one number to track for a month. Could be groceries, could be takeaways, could be your savings transfer. One number, every week, for four weeks.

- If you want a guided version of all of the above, join the Cozzy open beta.

Cozzy is a small Irish team trying to make money feel a little gentler — if that resonates, come and try the open beta, and please tell us what we got wrong.